Benefits of Leasing vs Buying at Fisher Honda

Many drivers start the shopping process focused on monthly cost, but the bigger decision often comes down to whether leasing or buying makes more sense for the way they actually drive. The benefits of leasing a car can be appealing for shoppers who want lower monthly payments, shorter commitment periods, and the opportunity to move into a newer Honda every few years. At the same time, buying may be the better fit for drivers who want long-term ownership and the ability to build equity in their vehicle.

This guide takes a closer look at leasing vs buying, how leasing works, and what shapes lease payments in the first place. We will also break down depreciation, ownership differences, end-of-lease options, and the situations where leasing may be the smarter choice. By the end, you will have a clearer understanding of the financial tradeoffs and which path may fit your lifestyle best.

Quick Answers

How does leasing a car work?

When you lease a vehicle, you make monthly payments to drive it for a set period, usually two to three years. Those lease payments are based largely on depreciation — the difference between the vehicle’s value when new and its expected value at the end of the lease.

Are lease payments usually lower than financing payments?

Lease payments are often lower than loan payments because you are paying only for the portion of the vehicle’s value used during the lease term. Financing a vehicle typically requires paying the full purchase price over time, which results in higher monthly payments.

What happens at the end of a car lease?

Most drivers have several end-of-lease options when the contract expires. You can return the vehicle, purchase it for the predetermined buyout price, or lease another new vehicle.

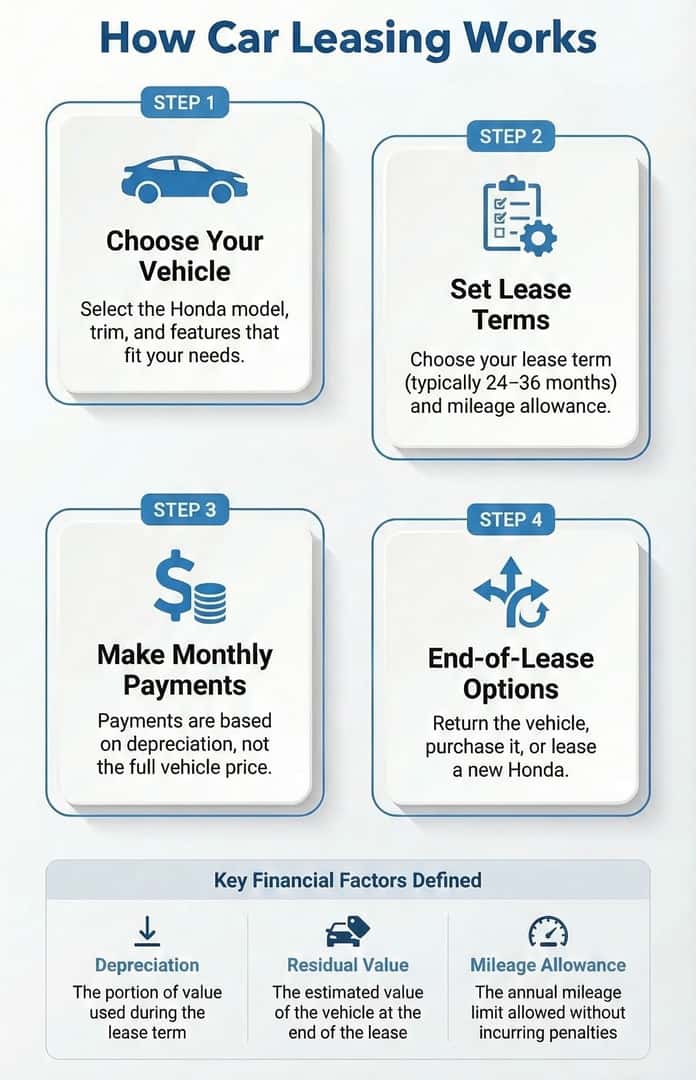

How Leasing a Car Works

Understanding how car leasing works starts with one key idea: when you lease a vehicle, you are paying for the portion of the vehicle’s value that you use during the lease term rather than the full purchase price. Lease payments are largely based on depreciation, which is the difference between the vehicle’s value when new and its expected value at the end of the lease. Because you are not financing the entire vehicle, lease payments are often lower than traditional loan payments.

In simple terms, a lease focuses on how much value the vehicle is expected to lose over time. For example, if a vehicle retains a strong portion of its value after three years, the depreciation amount is lower — which can result in more affordable monthly lease payments. This is one of the main reasons leasing can be appealing compared to financing the full purchase price.

A typical lease agreement outlines several important factors, including the lease term, mileage allowance, residual value, and the cost of financing the lease itself. Most leases run between 24 and 36 months, providing a predictable ownership timeline with clear expectations around usage and cost.

| Lease Payment Factor | What It Means |

|---|---|

| Depreciation | The portion of the vehicle’s value used during the lease term |

| Residual Value | The estimated value of the vehicle at the end of the lease |

| Lease Term | The length of the lease, typically 24 to 36 months |

| Mileage Allowance | The number of miles you can drive annually without penalties |

| Money Factor | The financing cost of the lease, similar to an interest rate |

| Capitalized Cost | The negotiated price of the vehicle used to calculate lease payments |

| Drive-Off Costs | Upfront costs that may include taxes, fees, and initial payments |

Each of these factors works together to determine your monthly lease payment. By understanding how depreciation, residual value, and financing costs interact, drivers can better evaluate lease offers and choose an option that fits their budget and driving habits.

Leasing vs Buying a Car: Key Differences

Many shoppers compare leasing vs buying a car when deciding how to pay for their next vehicle. Leasing and financing both allow you to drive a new vehicle with monthly payments, but the structure of the agreement and long-term financial impact are very different. Leasing typically focuses on short-term use and lower monthly payments, while buying involves paying off the full value of the vehicle over time and eventually owning it outright. The comparison below highlights the core differences between leasing and buying.

| Category | Leasing | Buying |

|---|---|---|

| Ownership | Return vehicle | Own vehicle |

| Monthly Payments | Usually lower | Usually higher |

| Equity | No equity | Builds equity |

| Mileage | Limited | Unlimited |

| Customization | Restricted | Allowed |

| End of Term | Return or buy | Keep vehicle |

The table above highlights the core structural differences between leasing and buying, but those differences often show up in more practical ways once you start thinking about day-to-day driving and long-term costs. Looking a little deeper at the benefits and potential drawbacks of leasing can help clarify when it makes sense—and when it might not—based on your budget, mileage, and overall driving habits.

The Biggest Benefits of Leasing a Honda

The benefits of leasing a car appeal to many drivers because the structure of a lease focuses on short-term vehicle use rather than long-term ownership. Instead of paying the full purchase price of a vehicle over time, leasing centers around depreciation — the portion of the vehicle’s value used during the lease term. This often results in lower monthly payments and makes it easier to move into a newer Honda every few years.

- Lower Monthly Payments:

Lease payments are usually lower than financing payments because they are based largely on depreciation rather than the full purchase price of the vehicle. That structure can make it easier for drivers to fit a new Honda into their monthly budget. - Drive a New Honda Every Few Years:

Leasing gives drivers the chance to upgrade more often, which means easier access to newer technology, updated safety features, and the latest model improvements without a long ownership timeline. - Warranty Coverage Throughout the Lease:

Most leased vehicles remain under the manufacturer’s warranty for the full lease term. This can help reduce unexpected repair costs and make ownership expenses feel more predictable. - Lower Upfront Costs:

Leasing often requires less money due at signing than purchasing. While there may still be drive-off costs, the upfront expense is often lower than a traditional down payment on a financed vehicle. - Flexibility at the End of the Lease:

When the lease ends, drivers typically have several choices. You may be able to lease another Honda, buy the current vehicle, or simply return it and move on to something else. - Access to Higher Trim Levels:

Because lease payments are often lower, some drivers find they can choose a higher trim level or more premium features than they would comfortably finance. - Potential Business Tax Advantages:

In some cases, leasing for business use may offer possible tax benefits. Because tax rules vary, drivers should speak with a qualified tax professional for guidance.

Potential Drawbacks of Leasing

At the same time, a balanced lease vs buy comparison should also account for the possible drawbacks. Leasing can provide flexibility and predictable costs, but it also comes with limitations that may not fit every driver. Looking at both sides together can make it easier to decide whether leasing matches your budget, mileage needs, and long-term ownership goals.

- Mileage Limits:

Most lease agreements include annual mileage limits, often around 10,000 to 12,000 miles per year. Drivers who go over the agreed allowance may owe extra mileage fees at the end of the lease. - No Ownership Equity:

Leasing does not build equity in the vehicle the way financing does. When you buy a vehicle, your payments gradually move you toward full ownership, while a lease typically ends with the vehicle being returned unless you choose a lease buyout. - Potential Fees & Charges:

Some lease agreements include charges for excess wear and tear, mileage overages, or end-of-lease processing. Depending on the contract, drivers may also encounter a disposition fee or early termination charges if the lease ends before the original term.

When Leasing May Be the Smart Choice

Many drivers comparing leasing vs buying want to know which option better fits their daily routine and financial priorities. Leasing makes sense in certain situations, especially for drivers who prefer predictable payments and the flexibility to upgrade vehicles more often while choosing from the latest Honda models available. While buying may be the better choice for long-term ownership, leasing can be an appealing option for drivers who value convenience, newer technology, and lower monthly payments. The scenarios below highlight when leasing may be a practical choice.

- Drivers who prefer upgrading to a newer vehicle every few years.

- People with shorter commutes who can comfortably stay within mileage limits.

- Budget-conscious drivers looking for lower monthly payments.

- Business owners who may use a leased vehicle for work purposes.

What Happens at the End of a Lease

As a lease approaches its final months, drivers typically begin reviewing their end-of-lease options. Most lease agreements outline the available choices in advance, making it easier to plan for the next step. Whether you want to continue driving a Honda, purchase your current vehicle, or simply return it, the end of a lease provides flexibility based on your needs and preferences.

- Lease another Honda: Many drivers choose to move into a new Honda with a fresh lease and updated features by browsing the latest Honda inventory and selecting a model that fits their needs.

- Return the vehicle: You can return the vehicle to the dealership and complete the lease without purchasing or starting another lease.

Why Drivers Choose Fisher Honda for Leasing

Drivers exploring Honda lease deals often want guidance from a team that understands both the vehicles and the leasing process. At Fisher Honda, our Honda-trained team helps drivers compare lease options, understand payment structures, and explore current Honda lease deals and specials to find an offer that fits their budget and lifestyle. Whether you are leasing a Honda for the first time or returning at the end of a previous lease, our staff focuses on clear explanations and straightforward support so you can move forward with confidence.

Shoppers from Boulder County, the Front Range, and nearby Northwest Denver communities visit Fisher Honda for a dealership experience that emphasizes transparency and expertise. Our team takes the time to walk through lease terms, available vehicles, and current offers so you can make an informed decision. From selecting the right model to reviewing your end-of-lease options in the future, Fisher Honda aims to make leasing simple and convenient.

FAQ: Leasing vs Buying A Car

3 comment(s) so far on Benefits of Leasing vs Buying at Fisher Honda

want to lease honda suv for daughter starting august please advise lease rates for 1 or 2 years , $ down down also list used car prices for smaller suv lot crv

Does Fisher Honda offer a 1 year Lease?

Looking to lease a civic for grandson

With low monthly